Does an EcoVadis score satisfy CSRD supply chain reporting requirements?

EcoVadis is widely used by EU companies to screen their suppliers. But CSRD imposes specific value chain data requirements that go beyond what EcoVadis was designed to collect. This article explains what CSRD actually requires, what EcoVadis provides, and where the gap is.

This article is for informational purposes only and does not constitute legal advice. Consult a qualified legal professional for advice specific to your situation.

The question EU procurement teams are asking

As CSRD reporting obligations have begun applying to large EU companies, sustainability teams and procurement functions have started asking a version of the same question: does requiring our suppliers to have an EcoVadis score mean we have covered our CSRD value chain requirements?

The short answer is: partially, and conditionally. EcoVadis data is relevant to some of what CSRD requires from value chain reporting. It is not sufficient for most of it, and for the area where CSRD imposes the most demanding and specific requirements, Scope 3 greenhouse gas emissions, EcoVadis provides almost nothing.

This matters for both sides of the supply chain. EU buyers who believe EcoVadis covers their CSRD exposure are operating with a gap that their assurance auditor will find. Non-EU suppliers who believe a good EcoVadis score means they have satisfied their buyer’s CSRD-related requirements may receive further requests they did not anticipate.

What CSRD requires from value chains

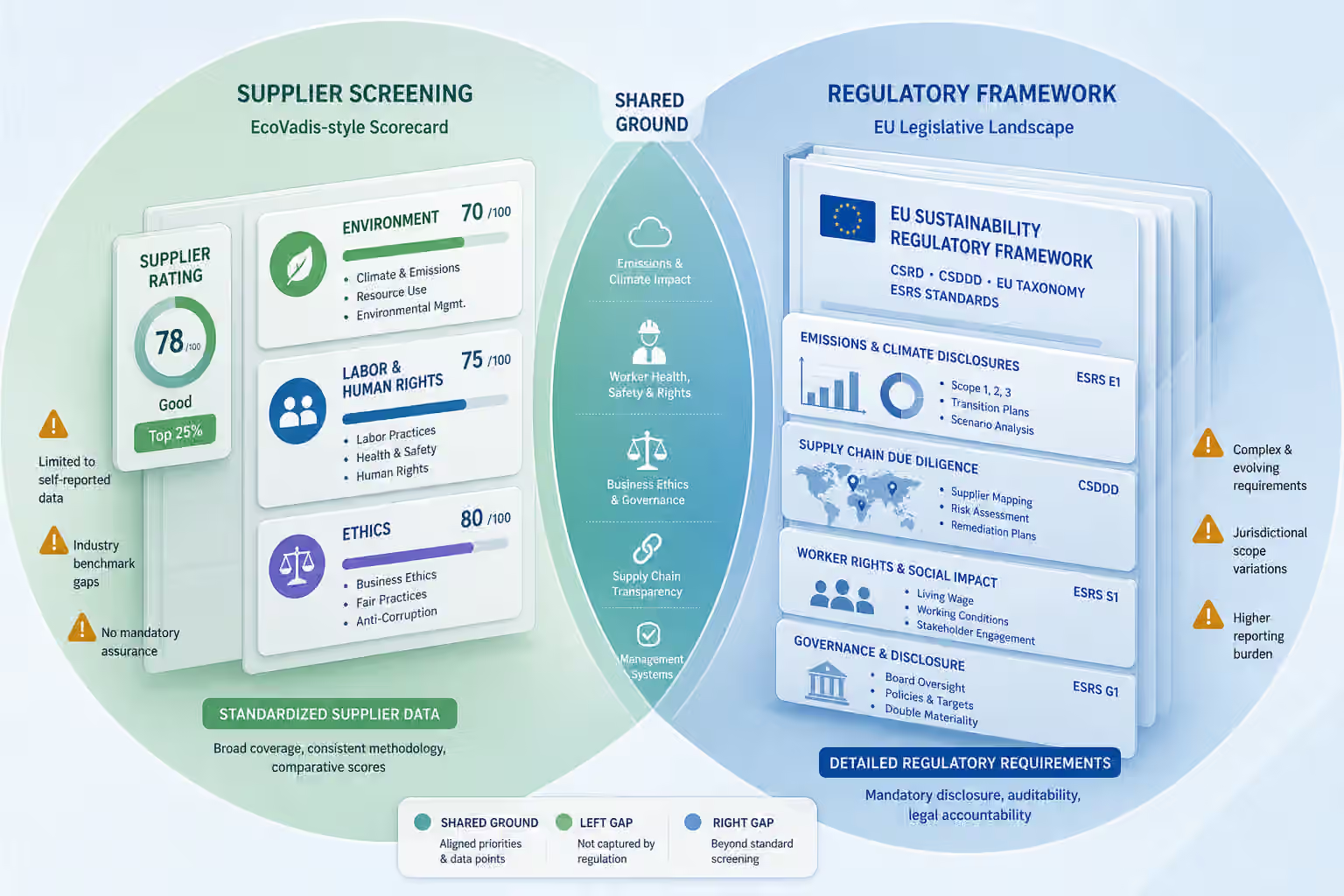

CSRD requires in-scope companies to report on sustainability matters across their own operations and their value chains, using the European Sustainability Reporting Standards (ESRS). The value chain scope under CSRD includes both upstream suppliers and downstream customers and end users.

The specific value chain data requirements vary by ESRS topic, but the most demanding and most commonly relevant are:

ESRS E1 (Climate): Companies must disclose their Scope 1, 2, and 3 greenhouse gas emissions. Scope 3 covers emissions from the value chain, including purchased goods and services (Category 1), upstream transportation and distribution (Category 4), and other categories depending on the company’s activities. For most manufacturers and retailers, Scope 3 Category 1 is the largest component of their total emissions footprint. Calculating it accurately requires emissions data from suppliers, either measured or estimated using spend-based or physical activity-based methods. The quality of Scope 3 reporting depends heavily on the quality of supplier-level data.

ESRS S2 (Workers in the value chain): Companies must disclose material impacts, risks, and opportunities relating to workers across their upstream and downstream value chains. This includes identifying adverse human rights impacts, describing due diligence processes, and reporting on outcomes. The required disclosures overlap with CSDDD obligations for companies subject to both regulations.

ESRS E4 (Biodiversity and ecosystems): For companies with material exposure to deforestation, land use change, or biodiversity impacts in their supply chains, this standard requires disclosure of those impacts and the measures taken to address them. Relevant industries include food, agriculture, textiles, and forestry.

ESRS G1 (Business conduct): Disclosures on corruption and bribery prevention, including in the supply chain, and on payment practices.

The cross-cutting standards ESRS 1 and ESRS 2 establish general requirements including the double materiality assessment, which determines which topical standards apply to a given company. Not all standards apply equally to all companies. But for most large manufacturers, retailers, and branded consumer goods companies, ESRS E1 climate disclosures with Scope 3 data and ESRS S2 value chain worker disclosures are both likely to be material.

What EcoVadis collects

EcoVadis collects information across four themes: environment, labour and human rights, ethics, and sustainable procurement. The questionnaire asks suppliers about their policies, actions, and management systems in each area. Scores are weighted toward documented evidence of actions and results rather than policy statements alone.

The environment theme covers energy and greenhouse gas emissions, water, biodiversity, and local pollution. The labour theme covers working conditions, health and safety, social dialogue, and human development. The ethics theme covers anti-corruption, anti-bribery, responsible information management, and fair competition. The sustainable procurement theme covers supplier relationships and responsible purchasing practices.

This is a broad framework that covers meaningful ground. For an EU buyer trying to get a general picture of where suppliers sit on ESG risk across a large portfolio, EcoVadis provides a standardised and scalable way to gather and compare that information.

Where EcoVadis falls short of CSRD requirements

Scope 3 emissions data

The most significant gap is on climate. ESRS E1 requires disclosure of Scope 3 emissions in physical units (tonnes of CO2 equivalent) broken down by category. For Category 1 (purchased goods and services), the preferred approach is supplier-specific data: actual emissions figures from the suppliers whose products and materials are purchased.

EcoVadis does not collect emissions data in this form. Its environment questionnaire asks suppliers whether they measure and report their greenhouse gas emissions, what reduction targets they have, and what actions they have taken. This generates information about the maturity of a supplier’s emissions management, not the emissions figures themselves.

A buyer reporting Scope 3 Category 1 emissions under ESRS E1 cannot use their suppliers’ EcoVadis environment scores as the data source for that calculation. They need actual emissions data: either supplier-provided activity data with emissions factors applied, or direct supplier-reported emissions figures. The CDP (Carbon Disclosure Project) climate questionnaire is a much more appropriate data source for this, and even CDP data often requires significant quality assessment before it can be used in assured Scope 3 calculations.

ESRS S2 value chain worker disclosures

EcoVadis collects information on labour standards that is relevant to ESRS S2. A buyer can use their suppliers’ EcoVadis labour scores as part of the information base that informs their double materiality assessment and their identification of material impacts in the value chain.

However, ESRS S2 requires more than a risk screening score. It requires disclosure of identified adverse impacts, the due diligence processes used to identify and address them, the effectiveness of those processes, and outcomes. This is qualitative, narrative disclosure supported by specific evidence, not a single numerical score.

An EcoVadis labour score can contribute to demonstrating that a buyer has a systematic approach to supplier assessment. It cannot by itself satisfy the disclosure requirements of ESRS S2, particularly the requirements to describe specific impacts identified and the actions taken in response to them.

Assurance implications

CSRD requires that sustainability reports be assured by an independent assurance provider. For the first years of reporting, limited assurance applies; the trajectory is toward reasonable assurance for larger companies.

An assurance auditor reviewing a company’s value chain data will assess the reliability and completeness of the information used. For Scope 3 emissions, they will look at the methodology used, the data sources, and the quality of supplier data. EcoVadis scores are based on self-assessed questionnaire responses reviewed by analysts: a commercially produced rating with acknowledged limitations around data verification. An assurance auditor is unlikely to accept EcoVadis environment scores as primary evidence for Scope 3 Category 1 calculations.

For ESRS S2, an assurance auditor will want to see evidence of due diligence processes, not just screening scores. EcoVadis provides a useful input but not the full evidentiary record that a well-documented due diligence process would produce.

What EcoVadis is genuinely useful for under CSRD

EcoVadis is most useful for the parts of CSRD that involve systematic supplier risk assessment and the identification of material sustainability topics in the value chain.

For the double materiality assessment required under ESRS 1, information about supplier ESG profiles helps companies assess where significant sustainability risks and impacts are concentrated in their supply chain. EcoVadis scores provide a structured basis for that analysis across large supplier portfolios.

For ESRS S2 and the general approach to value chain due diligence, EcoVadis can be part of a buyer’s evidence that they have a supplier assessment programme in place. Combined with other documentation of their CSDDD-aligned due diligence process, it contributes to the overall picture.

For identifying suppliers who need support or improvement, EcoVadis scores provide a tiering mechanism. Companies can prioritise engagement with lower-scoring suppliers as part of their supplier development approach.

These are real and useful contributions. The mistake is treating them as sufficient for CSRD compliance rather than as inputs to a broader compliance programme.

What the gap means for non-EU suppliers

For a non-EU supplier, the practical implication is this: even if you have a strong EcoVadis score, your EU buyer’s CSRD team may still ask you for additional information that EcoVadis does not collect.

The most likely additional request is for emissions data. If your EU buyer is reporting Scope 3 Category 1 emissions, they need activity data or emissions figures from their suppliers. They will either ask you to provide this directly, ask you to complete a CDP questionnaire, or use spend-based estimation methods that do not require data from you but produce less accurate results.

The second likely additional request is for more detailed labour and human rights information in support of their ESRS S2 disclosures, particularly if your sector or geography is associated with elevated risk and their materiality assessment has flagged value chain labour conditions as material.

Being prepared for these requests in advance, rather than encountering them as unexpected obligations after completing EcoVadis, puts you in a stronger position in your buyer relationships.

The broader compliance question

EcoVadis was built for procurement-facing supplier screening. CSRD was built for investor-facing and regulatory sustainability disclosure. The two overlap in some areas and diverge significantly in others.

A non-EU supplier trying to understand their compliance position under EU law needs to start from the legislation, not from a commercial ratings platform that predates the legislation and was not designed around it. The question of what CSRD supply chain obligations specifically require, and where your current practices create gaps, is a different question from what EcoVadis score you should aim for.

A detailed explanation of CSRD and the ESRS standards is available here: CSRD and ESRS explained: what the corporate sustainability reporting directive requires.

For a broader view of what CSRD requires from non-EU suppliers specifically, see: CSRD supply chain obligations: what non-EU suppliers need to know.

Verdandi monitors EUDR, CBAM, CSRD, CSDDD and more continuously — so non-EU businesses touching EU markets are working from current requirements as deadlines, benchmarks, and scope thresholds change. Start for free.

This article is part of a series on the supply chain sustainability platform landscape. See also: EcoVadis vs Sedex: which one does your EU buyer actually need?.

Every research tool claims traceability. Few mean the same thing by it. Here is what genuine traceability requires, what the weak versions look like, and why the difference matters when a finding is challenged.